lt;div style = "width:60%; display: inline-block; float:left; "> This post shows how to calculate a carry and roll-down on a yield curve using R. In the fixed income, the carry is a current YTM like a dividend yield in stock. But unlike stocks, even though market conditions remain constant over time, the r</div><div style = "width: 40%; display: inline-block; float:right;"><img src=

:max_bytes(150000):strip_icc()/termstructure.asp-final-531451909746444782a33d468bcb0246.png)

Term Structure of Interest Rates Explained

Global Macro Strategies: Volatility Carry Strategy with Swaptions

Brazilian Yield Curve

Riding the Yield Curve and Rolling Down the Yield Curve Explained

:max_bytes(150000):strip_icc()/Yield-Curve-6b685b5093f9425eada22cedf85d4d4f.jpg)

Yield Curve: What It Is and How to Use It

Carry and Roll-Down on a Yield Curve using R code

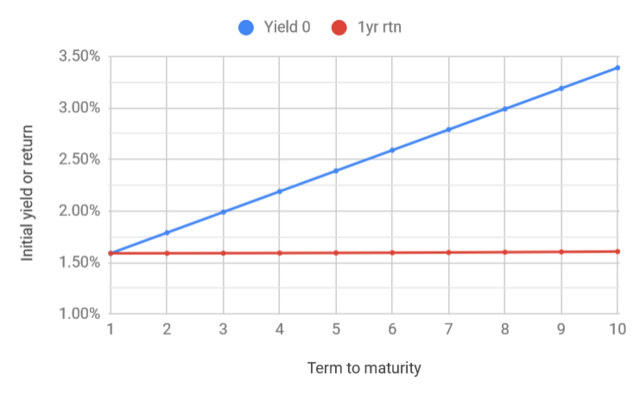

Yield curves and bond returns

Keep Calm and “Carry and Roll” On

How to calculate carry and roll-down (for a bond future's asset swap) –

Corporate bonds: Unraveling Roll Down Returns in Corporate Bond Portfolios - FasterCapital